Is AI a MUST or an OPTION? What a student’s Question Taught Me About How the World Actually Sees AI

Where this started

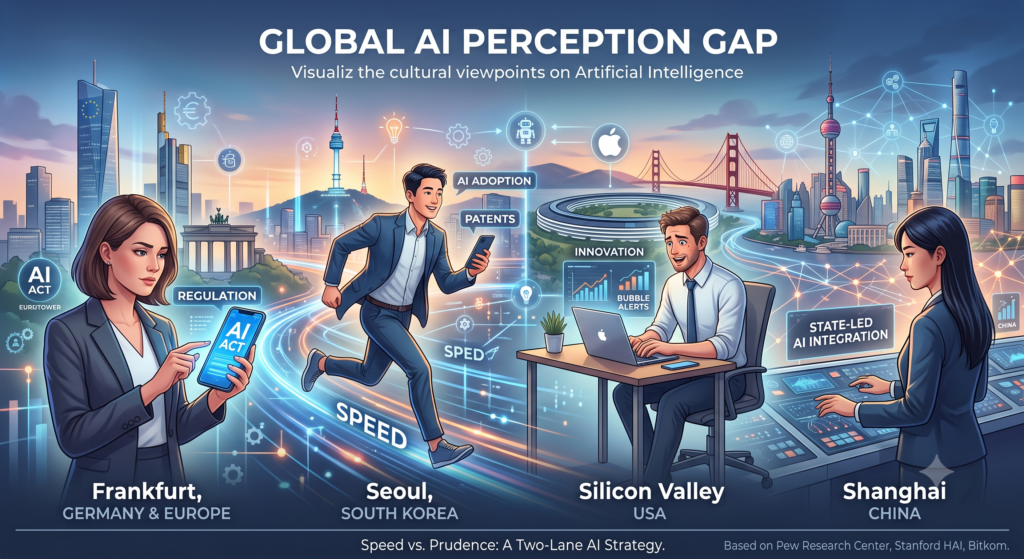

A few weeks ago, an IT Werkstudent (Working Student) at my company in Germany made me a simple comment: “Isn’t AI just a bubble?”

I was genuinely surprised. Not because the question was unreasonable, but because of where it was coming from. In Korea, AI has been the lead story in the news almost every day for the past three or four years. An entire generation of Korean university tech students has grown up with something close to AI FOMO — a real anxiety that if you’re not actively using AI, you’re already falling behind. So hearing a bright, capable university student in Germany calmly suggest the whole thing might be a bubble stopped me in my tracks.

That gap is what this post is about. Not who is “right,” but why two educated, connected populations can look at the exact same technology and arrive at such different conclusions — and what that tells us about how we should actually think about AI, as individuals, as companies, and as countries.

Two lenses on the same technology

The gap I noticed isn’t just anecdotal. A 2025 Pew Research Center survey of over 28,000 adults across 25 countries found that, on average, more people feel concerned about the growing use of AI (34%) than excited (16%), with the rest feeling a mix of both. South Korea was the clear outlier: only 16% of Koreans expressed more concern than excitement — the lowest of all 25 countries — while 61% said they feel a mix of both. Combine that with South Korea’s position as the world leader in AI patents per capita and one of the highest workplace AI adoption rates globally, and you get a population that is both unusually optimistic and unusually hands-on with the technology.

Germany tells a more divided story. Bitkom’s 2026 survey of German companies found that active AI use nearly tripled in two years — from 17% in 2024 to 41% in 2026. But that same survey found that one in three companies said AI had cost more than expected, and 19% had already cut jobs as a direct result. Germany, and Europe more broadly, has also leaned into regulation-first thinking: a majority of German companies surveyed say the EU AI Act creates more disadvantages than advantages for them. So the skepticism I heard from that Werkstudent isn’t irrational — it’s a fairly accurate reflection of what German companies themselves are reporting.

The United States sits somewhere else entirely: extreme enthusiasm and extreme bubble anxiety, coming from the same country at the same time. That contradiction is worth taking seriously, because it’s the most economically consequential version of this debate.

Checking the claim: are hyperscalers really taking on massive debt to fund this?

Yes — and the scale is larger than most casual conversations about it suggest.

The five largest hyperscalers (Amazon, Microsoft, Alphabet, Meta, and Oracle) are projected to spend around $602 billion on infrastructure in 2026, a 36% increase over 2025, with roughly 75% of that aimed at AI. To put that in context, one widely cited 2026 congressional briefing paper noted that hyperscaler AI capex for 2026 is on track to represent a larger share of U.S. GDP than the peak spending years of the Manhattan Project, the interstate highway system, or the Apollo program.

Not all of this is being paid for out of existing cash. In 2025, the five hyperscalers issued roughly $121 billion in new bonds — compared to about $40 billion in 2020. That pace accelerated further in early 2026: Oracle alone raised $25 billion in a single bond sale in February, and analysts at Morgan Stanley and JPMorgan estimate the broader tech sector may need to issue as much as $1.5 trillion in new debt over the next few years to keep funding AI infrastructure. Alphabet even issued a 100-year bond in February 2026 — the first tech company to do so in decades, which tells you something about how confident bond markets currently are that this spending will pay off eventually, even if not soon.

It’s important to note the companies are not equally exposed. Microsoft, Alphabet, and Amazon are financing this mostly from enormous existing cash flow and have balance sheets strong enough that even a serious misallocation of capital wouldn’t threaten their solvency. Oracle is the clear outlier — carrying debt levels that exceed Microsoft’s and Amazon’s in absolute terms despite a fraction of their revenue and equity cushion, which is why credit analysts have flagged it as the most fragile of the group.

So the Werkstudent’s underlying instinct — that enormous, debt-fueled spending is happening — is factually correct. Whether that spending constitutes a “bubble” is a separate, harder question.

Is it actually a bubble?

The honest answer is: parts of it look bubble-like, and parts of it don’t, and serious, well-informed people disagree.

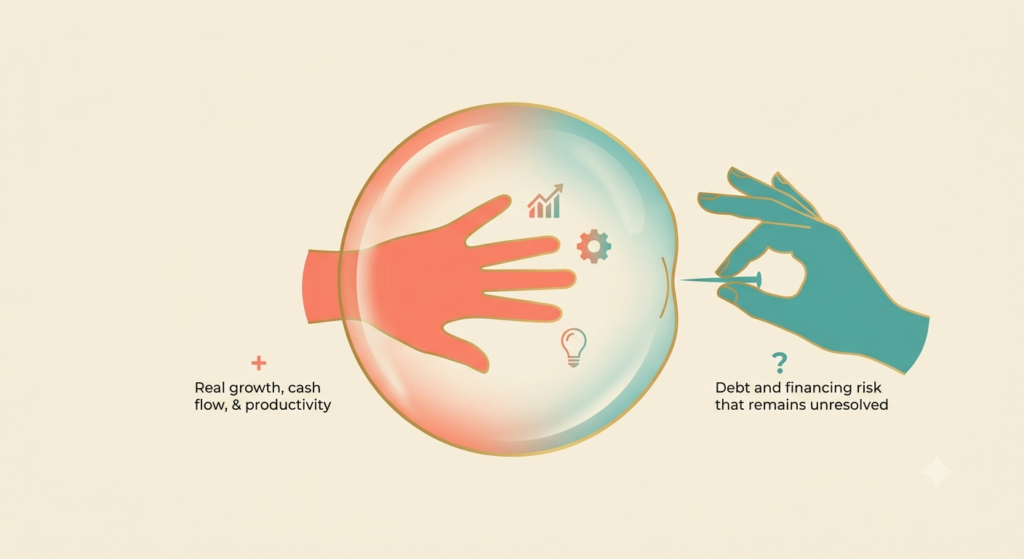

The case for “bubble”: Roughly 80% of S&P 500 gains in 2025 came from AI-related companies — an extreme concentration that historically precedes corrections. A significant share of reported AI revenue comes from circular financing arrangements — Nvidia invests in a cloud provider, which uses that capital to buy Nvidia chips, which shows up as revenue for both companies. The Bank for International Settlements (essentially the central bank for central banks) devoted a section of its 2026 annual report to warning that this spending is “outpacing earnings and free cash flow” at the hyperscalers, and compared it directly to historical episodes — canal mania, railway mania, the dot-com bubble — that all began as genuine technological breakthroughs and ended in recessions. On top of that, an MIT-linked study widely cited in 2025–2026 found that a striking share of enterprises running generative AI pilots report no measurable return so far.

The case against “bubble,” or at least “not yet”: Unlike the profitless dot-com companies of 1999–2000, today’s AI leaders generate real, growing cash flow — Nvidia posted about $216 billion in FY2026 revenue, up 65% year over year. Valuation multiples, while elevated, are meaningfully below dot-com extremes (Nvidia trades around 44–47x earnings versus Cisco’s roughly 200x at the 2000 peak). Enterprise adoption is also far broader and more embedded than internet adoption was in 1999: by 2025, most large enterprises had implemented generative AI in at least one function, and cloud AI revenue lines like Microsoft’s Azure AI are growing well over 100% year over year off a real, multi-billion-dollar base.

The most useful conclusion from people who study this closely isn’t “yes” or “no” — it’s that this is a genuine technology with genuine productivity gains, sitting inside a financing structure with real bubble characteristics. Those two things are not contradictory. They can, and probably do, both apply to what we’re watching happen in 2026.

So — is AI a MUST or an OPTION?

This is the question that actually matters for a person deciding how to spend their time, and I think the honest answer depends entirely on which layer of AI you’re talking about.

At the infrastructure and frontier-model layer — this is optional for almost everyone reading this. Whether Oracle can service its debt, whether the AI capex supercycle continues at $600+ billion a year, whether there’s a correction in 2026 or 2029 or never — these are questions for investors, policymakers, and hyperscaler executives. You do not need a position on whether Nvidia is overvalued to benefit from AI in your own work.

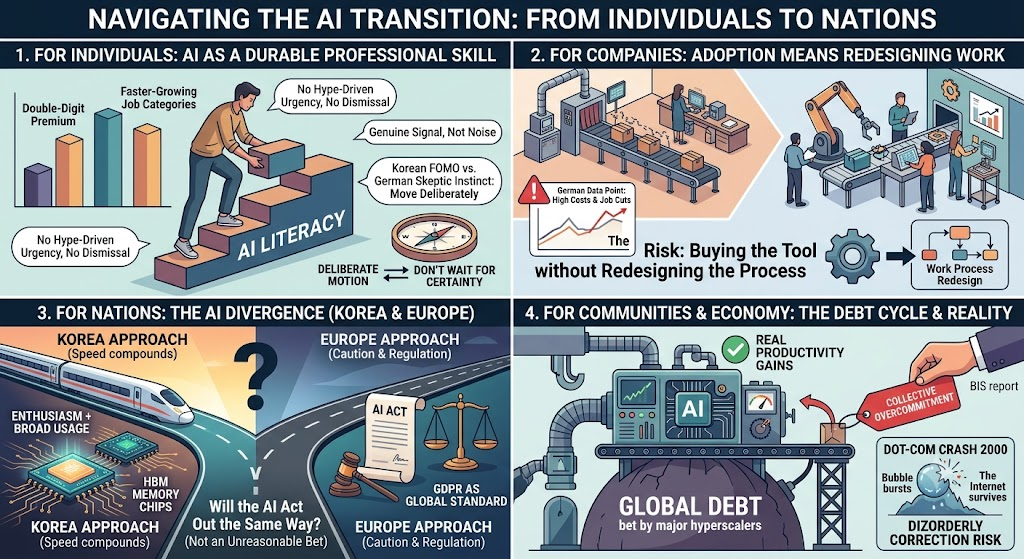

At the individual skills layer — the evidence increasingly points to MUST, not OPTION. This is really the useful, separate question hiding inside “is AI a bubble.” PwC’s 2026 Global AI Jobs Barometer, which analyzed more than a billion job postings across 27 countries, found that workers with AI skills now earn a 62% wage premium over peers, up from 57% the year before. The World Economic Forum expects 39% of workers’ core skills to change by 2030. This doesn’t mean everyone needs to become a machine learning engineer — PwC’s data actually shows the biggest wage and hiring gains going to people who combine AI fluency with human judgment, communication, and domain expertise, not people who out-technical the tool. But treating AI literacy as skippable now looks like treating spreadsheet literacy as skippable in the 1990s.

At the enterprise layer — it’s closer to MUST, but with a large asterisk. Adoption is now mainstream (87%+ of large enterprises use generative AI in some function), but the same data shows most projects aren’t yet returning clear value — one widely cited MIT-linked estimate put the “zero measurable ROI” share of enterprise GenAI pilots as high as 95%. So the honest enterprise-level answer is: not adopting is increasingly not a viable option, but adopting badly, without redesigning workflows around it, is nearly as common a failure mode as not adopting at all. Deloitte’s 2026 research found only 6% of leaders feel they’re making real progress on actually redesigning how humans and AI work together — meaning most of the current spending on AI adoption is still fairly poorly targeted.

What this means for different actors

For individuals: Build AI literacy the way you’d build any durable professional skill — not out of hype-driven urgency, and not out of dismissal, but because the wage and hiring data are now large enough (double-digit premiums, faster-growing job categories) to treat as a genuine signal rather than noise. The Korean FOMO instinct and the German skeptic instinct are both partially right here: move deliberately, but don’t wait for certainty before starting.

For companies: The risk isn’t in adopting AI or in avoiding it — it’s in adopting it without changing how work actually gets done around it. The German data point about companies cutting staff after AI costs came in higher than expected is a useful cautionary tale: it suggests some organizations bought the tool without redesigning the process, then treated headcount as the adjustment variable when the ROI didn’t show up on schedule.

For nations: This is genuinely a fork.

Korea’s approach — enthusiasm plus fast, broad real-world usage plus strength in patents and hardware supply chains (HBM memory in particular) — is a defensible bet on capturing upside in a race where speed compounds.

Europe’s approach — caution, governance-first regulation, and skepticism about ROI — has a real historical precedent for eventually paying off: GDPR was initially seen as a competitive handicap for European firms and later became a global compliance standard that European companies were simply more prepared for than their competitors elsewhere. Whether the AI Act plays out the same way is an open question, but it’s not an unreasonable bet.

China’s approach is different again: rather than racing for frontier capability or racing to regulate first, it’s racing to deploy — cheaper models, mandated adoption targets, and a financing structure that’s largely insulated from the U.S. hyperscaler debt story, at the cost of betting heavily on state-directed capital allocation and an increasingly separate hardware ecosystem. Three genuinely different national bets, running at the same time, is arguably the most interesting part of this entire story.

For communities and the broader economy: This is where the debt story actually matters most, and it’s the one place where “is it a bubble” stops being an abstract argument. The BIS’s specific worry isn’t that AI is fake — its own report explicitly credits AI with real, measurable productivity gains. Its worry is that every major hyperscaler is making the same enormous, debt-financed bet simultaneously, on the assumption that only a few players will end up dominating. That’s a classic setup for collective overcommitment: even if AI itself is completely real and valuable, the current financing structure around it could still produce a disorderly correction that hits jobs, credit markets, and unrelated sectors on the way down — which is exactly what happened after the dot-com crash, even though the internet itself turned out to be very real.

Where I’ve landed

Separate the technology from the financing, and separate the infrastructure question from the personal one.

The technology is real. The productivity gains, while uneven, are measurable and growing. The financing structure funding the current buildout does show real bubble characteristics — concentration, circular deals, spending that’s outpacing hyperscaler cash flow — and a correction at some point would not be shocking to serious economists at the BIS, JPMorgan, or elsewhere.

But none of that changes the individual-level answer much. Whether or not Oracle’s balance sheet survives the next two years, becoming fluent enough with AI to use it well in your own work is no longer a hedge against hype — it’s closer to a baseline professional skill, the way basic digital literacy became one in the 2000s. The Werkstudent’s skepticism about the market may turn out to be well founded. That’s a completely different question from whether they should be learning to use the tools right now. On that second question, the data isn’t really ambiguous.

Sources: Pew Research Center (2025 25-country AI survey); Bitkom 2026 AI study; CreditSights and Introl hyperscaler capex/debt estimates; Bank for International Settlements Annual Economic Report 2026; Fortune, Reuters/Yahoo Finance and Mawer Investment Management reporting on hyperscaler bond issuance; PwC 2026 Global AI Jobs Barometer; MIT-linked enterprise GenAI ROI research; Deloitte 2026 Global Human Capital Trends; Wikipedia’s “AI bubble” summary of the wider debate (Ray Dalio, Michael Burry, Goldman Sachs, Morgan Stanley, and others); Stanford HAI 2026 AI Index Report (public opinion chapter); Fortune and Janus Henderson reporting on China’s AI deployment strategy; U.S.-China Economic and Security Review Commission report “Two Loops: How China’s Open AI Strategy Reinforces Its Industrial Dominance”; DigitalinAsia analysis of China’s 15th Five-Year Plan AI targets.

#AIbubble, #ArtificialIntelligence, #AIskills, #Korea, #Germany, #Hyperscalers, #Futureofwork,#ViewonAI