From the Paradigm Shift Since the Industrial Revolution to the Trap of “Cheap,” and the Tasks Facing Individuals, Companies, Nations, and the Environment — A Consolidated Report

Prepared: July 11, 2026

Introduction

This piece started from a simple observation and grew into something bigger through a series of questions, each one built on the last:

1. Is the world re-localizing manufacturing, even at higher cost — and what does that mean for globalization? The starting point was a hunch: that nations are pushing to bring manufacturing home for their own benefit, even if it costs more, and that physical AI (robotics) might become the next core variable of national manufacturing competitiveness. That raised an immediate irony — most robots at the world’s largest robotics competition were Chinese, and Apple was reportedly lobbying to use Chinese memory chips. If cost-efficiency still drives the game, what does that mean for the future of globalization itself?

2. But is “cheap” really sustainable — or is it an illusion? That led to a harder question: given today’s exploding AI-driven demand for chips, can Chinese semiconductors actually stay cheap? Digging into the numbers revealed a twist — they’re not cheap right now at all. Which reframed the whole inquiry: is “cost-efficiency” a real market outcome, or a state-subsidized illusion with a limited shelf life?

3. What does this mean for everyone — not just states and corporations? Once the state-vs-corporate tension was clear, the next question was who else is affected. What is asked of individuals, governments, companies, families, and communities in this realignment? How do economists evaluate it, and how does it need to reconcile with environmental change — particularly the energy demands of AI and reshored manufacturing?

4. What does “global realignment” even mean, in plain terms? Before going further, it became clear the term itself needed defining — not as jargon, but as a concrete historical shift: from “cheapest wins” (1990s–2008) to “trusted and secure, even if pricier” (2018–today), driven by three shocks — the US-China trade war, COVID supply breaks, and the Ukraine war.

5. Who actually pays for this — and what does “the bill” really mean? Finally, once the costs were framed as an “invoice,” the natural follow-up was: what does that metaphor actually cash out to? Who pays, and in what form — higher prices, lost growth, taxpayer subsidies, wage disruption, regional decline, or energy infrastructure?

Together, these questions move from a single observation (reshoring + robots + Apple’s chip lobbying) to a full picture: a historical reframing of globalization, a reality check on “cheap,” and finally a concrete accounting of who bears the cost of this transition — governments, companies, individuals, families, communities, and the environment alike.

Executive Summary

This report diagnoses where we currently stand within the recurring tides of globalization since the Industrial Revolution. It makes three core arguments.

First, today’s “manufacturing localization” trend is not an ideological victory but a recalculation of risk and cost. Second, physical AI (robotics) has emerged as a core variable in next-generation manufacturing competitiveness on top of this trend, but the substance of that competitiveness lies not in market efficiency but in state-led industrial policy and capital endurance — the case of Apple and the Chinese chipmaker CXMT illustrates this precisely. Third, this realignment is never free, and its costs are being distributed unevenly across nations, companies, individuals, families, and communities, compounded further by the environmental variable of surging AI-driven energy demand.

Economists’ overall assessment is consistent: “The shift from efficiency to resilience is not a question of right or wrong, but a question of cost — and if that cost is not deliberately distributed, society quietly but surely fractures.”

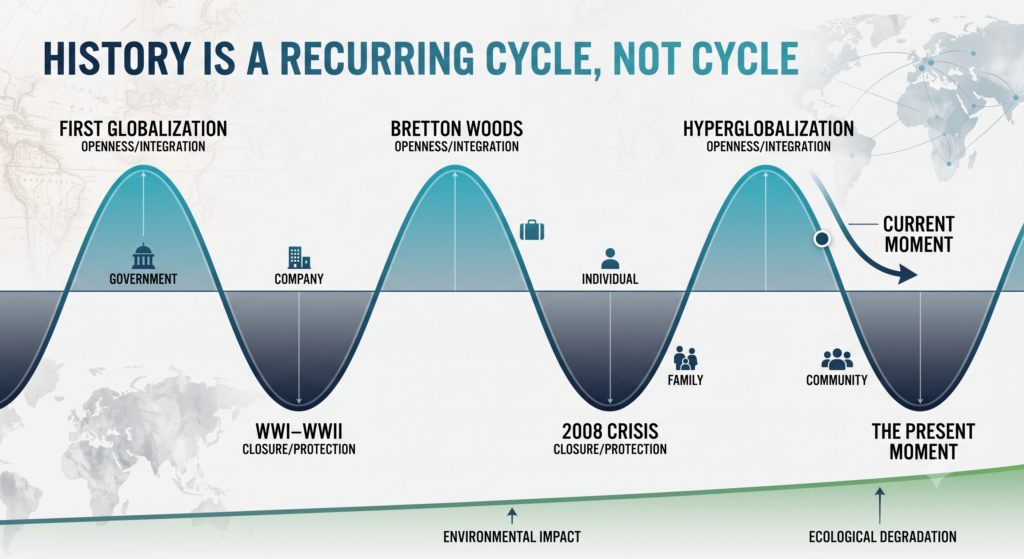

1. The Big Picture — Waves of Globalization Since the Industrial Revolution

The world economy has never moved in a straight line since the Industrial Revolution. It has swung back and forth between liberalization and protectionism like a tide.

1.1 First Globalization (Late 19th Century – 1914) Steamships, railways, the telegraph, the gold standard, and comparatively low tariffs combined to open the first era of free cross-border movement of capital, goods, and labor. This system collapsed with the First World War.

1.2 Collapse and Protectionism (1914 – 1945) Two world wars, the Great Depression, and protectionism epitomized by the Smoot-Hawley Tariff Act caused global trade to contract sharply. Economic nationalism and self-sufficiency dominated the discourse.

1.3 Bretton Woods and Managed Liberalization (1945 – 1970s) The GATT system, the Bretton Woods fixed exchange-rate regime, and the Marshall Plan enabled gradual, managed trade liberalization within the Western bloc, while the Cold War divided the world economy along ideological lines.

1.4 Neoliberal Hyperglobalization (1980s – 2008) Deregulation, capital-market opening, the founding of the WTO (1995), and especially China’s WTO accession (2001) pushed offshoring and global supply-chain fragmentation to their peak. Efficiency and cost minimization became the dominant values.

1.5 The First Cracks (2008 – 2016) The Global Financial Crisis intensified income inequality and manufacturing hollowing-out in advanced economies, and Brexit along with the 2016 U.S. election gave protectionist sentiment new political force.

1.6 Deglobalization and Realignment (2018 – Present) The U.S.-China trade war, COVID-19 supply-chain disruptions, renewed awareness of energy and food security from the Russia-Ukraine war, and industrial policies such as the CHIPS Act and the Inflation Reduction Act have pushed “resilience” and “security” — not just efficiency — to the center of supply-chain design.

2. The Current Paradigm — Not Ideology, but the Repricing of Risk

The current movement cannot be explained by the traditional divide between free trade and protectionism. It looks more like the pandemic, war, and the technology rivalry exposing supply chains’ previously hidden costs — stockouts, geopolitical hostage risk tied to specific countries, and dependence on single-source critical components. As a result, companies and nations are shifting their decision criterion from pure cost minimization to a composite goal of cost + resilience + security. Reshoring, nearshoring, and friend-shoring can be understood as a kind of insurance premium willingly paid to achieve that composite objective.

3. The New Variable — Physical AI and the Next Stage of Manufacturing Competitiveness

There was an expectation that advances in robotics and embodied AI would neutralize labor-cost gaps and bring manufacturing back to advanced economies. Current data, however, points in nearly the opposite direction. As of 2026, roughly 90% of humanoid robots sold worldwide are Chinese-made, with companies like Unitree and Agibot dominating the market by a wide margin.

RoboCup 2026, held in Incheon in July 2026 — the world’s largest robotics competition — illustrates this symbolically. With more than 3,000 participants from 45 countries, over 70% of participating teams used humanoid platforms from China’s Booster Robotics. Of 59 teams in the humanoid leagues, 38 competed on this company’s robots, and Booster-based teams swept gold, silver, and bronze across the board. In effect, research teams from the U.S. and elsewhere were not competing on their own national robot hardware, but on proven Chinese hardware, layering their own software and AI on top.

This suggests that competitiveness in physical AI itself is being built on the extension of a traditional Chinese industrial strategy — “low-cost mass production capacity + massive real-world data accumulation.” One interpretation is that robots are not replacing human labor, but that a new form of low-cost, labor-intensive industry — robotics — is re-emerging.

4. Revisiting the Irony — The Apple/CXMT Case and the “Trap of Cost-Efficiency”

4.1 The Surface-Level Irony: Even Apple Crosses Borders In the first half of 2026, as AI-data-center demand drove DRAM and NAND prices sharply higher (some contract prices reportedly rose more than 60% quarter over quarter), Apple raised Mac and iPad prices by 17–25%. At the same time, Apple was reportedly lobbying the U.S. government for approval to source chips from ChangXin Memory Technologies (CXMT), a Chinese DRAM maker on the Pentagon’s “1260H list” of companies suspected of ties to the Chinese military. Most analysts interpret this as a leverage play against Samsung, SK hynix, and Micron rather than a genuine switch.

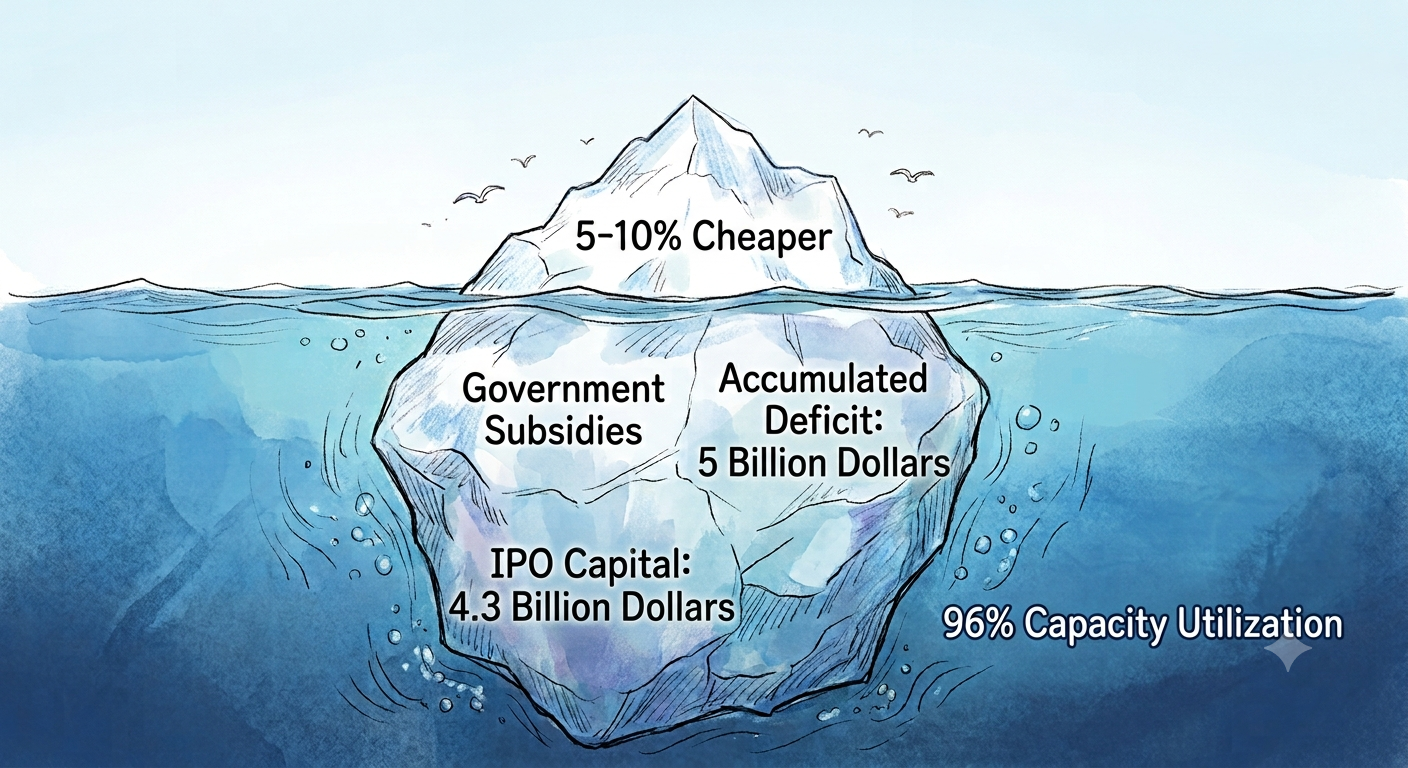

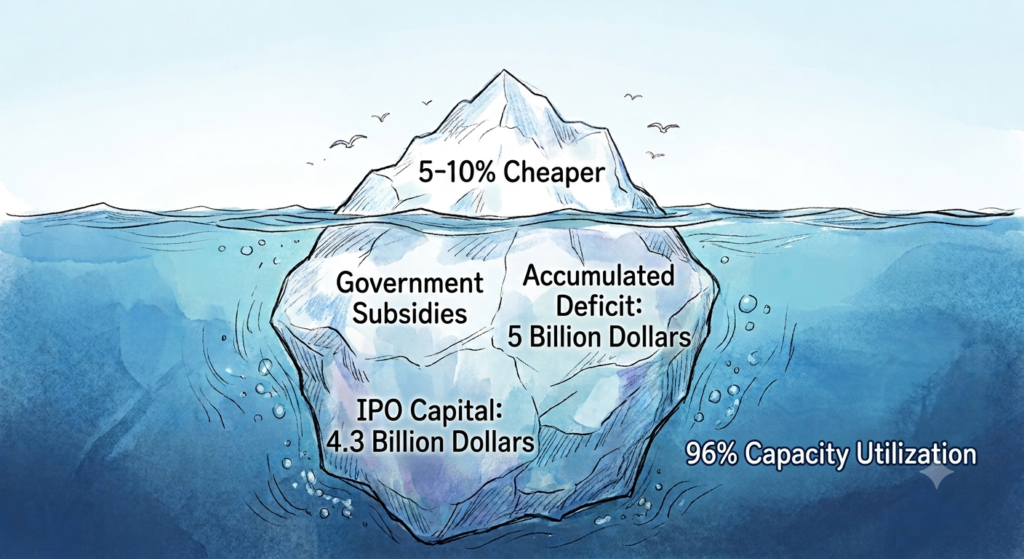

4.2 The Twist: Chinese Chips Are Not Cheap Right Now At All A closer look at the data shakes the very premise that “Chinese chips = cheap.” CXMT’s prices are only 5–10% below the three major manufacturers — far from anything resembling “dumping.” Its fab utilization is already at roughly 95.73% (as of 2025), essentially full capacity, leaving little spare capacity to unleash. In fact, the company posted net profit of roughly RMB 3.3 billion in Q1 2026 alone, with first-half profit projected to reach as much as RMB 57 billion — enough to wipe out eight years of accumulated losses (RMB 36.6 billion) in half a year.

In other words, this is not a case of “China selling cheap so Apple benefits.” Rather, it’s a moment when global chip prices have surged due to AI demand, and Chinese firms are cashing in on the same high-profit cycle as everyone else.

4.3 The Real Substance Behind the “Cheap” Image — The Endurance of State Capital CXMT raised roughly ₩4.3 trillion (about $3.1B) through its IPO to expand monthly production from 300,000 wafers today to 420,000 by 2027 and 500,000 by 2028. Sustaining this level of capital expenditure requires capital on the scale of Micron, Samsung, or SK hynix every year — yet CXMT is a company that accumulated roughly ₩5 trillion in losses over eight years, and could not have reached this point without state capital and policy financing. Ultimately, the substance of “cost-efficiency” is not market-validated cost competitiveness, but a question of how long a state is willing to absorb losses while continuing to inject capital.

5. The Structure of Conflicting Needs Between Companies and Governments

- The State (U.S.): Wants to contain CXMT on security grounds, but is under dual pressure to also protect domestic consumer prices and corporate competitiveness.

- The Company (Apple): Prioritizes cost, supply stability, and negotiating leverage over security logic — CXMT functions as a bargaining chip.

- The State (China): Treats semiconductor self-sufficiency as a national strategy and pours massive capital into CXMT — closer to policy-driven support fire than market competition.

- The Companies (Samsung, SK hynix, Micron): In a supercycle, they don’t fear CXMT much and are enjoying room to raise prices.

These four actors’ interests happen to align at this particular moment, but structurally, they are looking in different directions.

6. Economists’ Overall Assessment — “This Is Not Free”

- WEF (June 2026): Geoeconomic fragmentation is already costing the world economy $213–307 billion annually. Under a severe scenario, losses could reach 6.4% of global GDP (up to $6.9 trillion).

- WTO Secretariat: Full bifurcation into blocs could cost up to 7% of global real GDP.

- IMF: Strategic decoupling could cause a permanent loss of roughly 0.3% of global GDP (equivalent to Norway’s annual economic output).

- Wage impact in the U.S.: Low-skilled -0.33%, mid-skilled -0.49%, high-skilled -0.66% — a paradox where higher skill levels face greater impact.

- Countries outside major blocs could face a 10.7% GDP hit, far above the global average.

7. Tasks and Roles by Stakeholder

| Stakeholder | Core Task |

|---|---|

| Governments | Design industrial policy and social safety nets together; place-based policy tailored to regions |

| Companies | Solve the composite equation of cost + resilience + security; redesign human-AI collaboration; energy sourcing strategy |

| Individuals | Make lifelong learning the default — 59 of every 100 workers will need reskilling by 2030, 11 at risk of never getting the chance |

| Families | Build financial buffers against income volatility; redistribute roles and knowledge across generations |

| Communities | Invest in regional resilience so that feeling “left behind” doesn’t turn into a collapse of trust |

8. Reconciling With Environmental Change

Manufacturing reshoring and the spread of physical AI are driving explosive energy demand. Data-center electricity demand is projected to rise from 945 TWh in 2030 to 1,200 TWh by 2035. Ireland already draws 21% of its total electricity for data centers, and the U.S. state of Virginia draws 26%.

Two opposing outlooks exist: (1) An optimistic view — renewables will cover most of the increase in data-center power through 2035, with fossil fuels accounting for only about 15%. (2) A pessimistic view — even by 2030, roughly 40% of the increased demand will still be met by gas and coal, making data centers one of the few sectors whose emissions keep rising even as other industries decarbonize.

This is a point where the logic of national security/self-sufficiency and climate goals could collide head-on.

9. Overall Conclusion and Outlook

Since the Industrial Revolution, the world economy has traced a grand cycle: liberalization → collapse/protectionism → managed liberalization → hyperglobalization → fracture. The current trend is not a complete “deglobalization,” but a selective realignment in which the strategic sector (advanced semiconductors, defense/security AI — reorganizing along blocs, security-first) and the commodity sector (consumer goods, general-purpose components — still governed by cost logic) move according to different logics.

Economists’ message converges on one point: the shift from efficiency to resilience is not a question of right or wrong, but a question of cost — and if that cost is not deliberately and fairly distributed, society will quietly but surely fracture.

Sources: RoboCup 2026 organizing committee, TrendForce, Notebookcheck, MacRumors, World Economic Forum, WTO Secretariat, IMF, OECD, IEA, Carbon Brief, and other 2026 reporting and research.

Tags

#Globalization #Deglobalization #Reshoring #FriendShoring #PhysicalAI #Robotics #RoboCup2026 #Semiconductors #CXMT #Apple #Samsung #SKHynix #Micron #SupplyChain #IndustrialPolicy #Geoeconomics #FutureOfWork #ClimateAndEnergy #EconomicHistory #WEF #IMF